THIS MATERIAL IS A MARKETING COMMUNICATION.

Monthly Commentary on Key Themes – April 2024

China and Asia Semiconductor

Industry Update

- Asia supply chain plays a key role in Nvidia’s next-generation AI Processor: Nvidia introduced the Blackwell AI Processor at the GTC Conference, extending its leadership in AI computing. Nvidia said the new B200 GPU offers up to 20 petaflops of FP4 horsepower from its 208 billion transistors. GB200 which combines two of those GPUs with a single Grace CPU can offer 30 times the performance for LLM inference workloads, while also potentially being substantially more efficient. It reduces cost and energy consumption by up to 25 times over an H100, according to the company.1

- Asia semiconductor supply chain will play a key role in the supply of the new Blackwell platform, in fact majority of the supply chain for this platform from chip level to server and rack level is located in Asia. TSMC will be the foundry partner to produce the Blackwell processors, while SK Hynix is the major supplier in HBM (high bandwidth memory) for the chip.

- Samsung announced preliminary results: Samsung Electronics announced its 1Q24 preliminary earnings before the market opened on 5 April. It posted revenue of KRW71.1tn (+5% QoQ, +11% YoY) and operating profit of KRW6.6tn (+134% QoQ, 9x YoY) in 1Q24, which was much higher than market estimates, driven by the memory business.2

Stock Comments

- NAURA (+7.97%): Naura is a key local semiconductor equipment supplier in China. The company announced strong 4Q23 preliminary results, 4Q23 earnings of RMB 996mn at the midpoint up 49% YoY was well ahead of street expectations. Management also remains optimistic about WFE spending in China driven by both logic and memory capacity expansion.3

- Will Semi (+2.60%): Will Semi is one of the top 3 smartphone CIS suppliers globally. CIS inventory levels are now relatively healthy after destocking in 2023. The company is expected to gain market share in the flagship segment with the launch of competitive CIS models like the 50H. Overall recovery in smartphone shipment will also drive CIS industry demand.4

Preview

Increasing AI adoption in the data center and increasing penetration of AI at the edge and on-device will be the key enabler of the next upcycle semiconductor as AI-enabled devices have much higher semi-content. Currently, we are still in the process of cycle recovery as both stocks and earnings are below the previous peak. We expect volume growth in end devices to drive broad-based semiconductor cycle recovery in 2024.5

China Robotics and AI

Industry Update

- China Machinery Industry Federation (CMIF): Machinery industry profit up 7.5% YoY to RMB 166.6bn in Jan-Feb. According to the latest data of CMIF, machinery industry revenue was RMB 3.9tn in Jan-Feb, up 3.3% YoY; machinery industry profit was RMB 166.6bn, up 7.5% YoY.6

- China Customs: 3D printing equipment export volume of 3.5mn units in 2023, up 88% YoY. According to the customs, 3D printing equipment export volume of 3.5mn units in 2023, up 88% YoY. Meanwhile, the 3D printing export value of RMB 6.2bn up 68.5% YoY.7

- Zhejiang Dingli Machinery: Announced capacity expansion in China. Dingli announced a capacity expansion for its electric AWP (aerial working platform) in Zhejiang with RMB 1.7bn capex, from its own cash. The company had RMB 3.2bn net cash at the end of 3Q23.8 Our take - neutral: We think the expansion will have little impact in the near term, but the new capacity coming from the company's own cash indicates management confidence in AWP demand and Dingli's competitiveness.

Stock Comments

- Baidu (+4.69%): According to the WSJ, Apple has been in preliminary discussions with Baidu about adopting Ernie LLM (large language model) in Apple devices in China – though such discussions are still exploratory, and it is unknown whether Apple has been engaging with other local generative AI companies at this stage.9

- Zuzhou TFT Optical (+11.63%): The company is a component supplier for Nvidia’s optical transceiver. Data center bandwidth upgrade drives demand for optical modules. AI-accelerated optical module upgrades drive rapid growth in high-speed optical module TAM.

Preview

The industry continues to innovate and bring AI to the edge, we expect increasing AI capabilities in PCs and smartphones. In China, domestic LLM suppliers see increasing demand to offer customized AI capabilities on upcoming domestic hardware. New energy demand slumped further in March but a recovery is emerging in traditional industries, led by consumer electronics. Whether this is because of seasonality in March post-CNY needs to be closely watched.

China Electric Vehicle and Battery

Industry Update

- Accelerating EV sales in March; EV penetration on the rise: According to CPCA estimates, March passenger NEV wholesale reached 820k, +33% YoY and +84% MoM.10 Based on the announcements of individual auto brands, BYD reported March NEV sales of 302k units, +46% YoY, driven by the solid sales momentum of "Honor" facelifts since late February with minor spec upgrades but meaningful price cuts of 10-20%. Overseas sales up 65% MoM to a record level of 38.4k units. Other major EV brands, including Li Auto (+39% YoY), NIO (+14% YoY), and Xpeng (+29% YoY), all recorded accelerating growth in March delivery. Based on insurance registration, new energy vehicle (NEV) penetration was 43.7% in the last week of March, +1.2ppt MoM.11

- Battery inventory cycle bottoming out: According to the China Automotive Battery Innovation Alliance (CABIA), China’s EV battery installation was 17.9 GWh in February, down 45% MoM. EV battery inventory is in a continuous destocking cycle and there are signs of bottoming out, with global battery inventory months dropping significantly to 1.1 months in Jan 2024 from 3.5 months one year ago. CATL continues to expand market share, with domestic installation share rising 6ppts MoM in February, to 55%, while BYD’s share declined sequentially to 18%.

- Battery material costs rebounded in March: China’s spot lithium carbonate price was around RMB 112.3k/t at the end of March, +17% MoM12, driven by a pickup in downstream scheduled production demand and short-term disruption in supply.13 Inventory-wise, the total inventory of lithium carbonate came in at 77,815 tons, -3% YoY.14

- Strong launch for Xiaomi SU7; Momentum continued for Huawei AITO: On 28 March, Xiaomi launched its first EV model SU7 with price ranges between RMB 215.9k and RMB 299.9k, and received record-high 89k deposits within 24 hours. Considering the potential refund by customers, SU7 could reach 100k units in 2024 total sales and become one of the best-selling premium EV sedans in China, comparable to the Tesla Model 3.15 The AITO brand deliveries reached 31,727 units in March (+50% MoM), with new AITO M7 deliveries at 24,598 units, +33% MoM.16

- Increasing promotions to drive accelerating 2Q EV sales: Following Xiaomi’s SU7 launch, major local EV brands kick-started peak sales season with new rounds of promotion campaigns, which, coupled with recovering store traffic and supportive policies, should drive accelerating sales in 2Q.17 However, the rich product pipeline in 2024 and the subsidies/price cuts introduced by major brands could lead to prolonged price competition, which will undermine the profitability of EV brands.

Stock Comments

- BYD (002594.CH): BYD’s share price was up 9% in March, a positive contributor to the index. BYD reported in-line 4Q23 results with net profit growing +19% YoY18. Net profit per car dropped by 16% YoY but is still decent despite industry price competition,19 thanks to economies of scale, supply chain integration, and increasing contribution of premium brands and exports. Notably, BYD has an unprecedented R&D team of ~100k engineers20, the largest among global carmakers, which should support its continued technology innovation. We are seeing more emphasis on BYD’s intelligent driving development that will elevate user experience and enhance competitive advantages. The dividend payout ratio increased to 30% of earnings, from 20% last year.

- CATL (300750.CH): CATL’s share price was up 16% in March, a positive contributor to the index. CATL posted better-than-expected 2023 results and raised the dividend payout ratio to 50% (2.8% yield) from 20% in 2022, delivering better shareholder returns. Several leading sell-side institutions upgraded CATL’s ratings on its strong cash-generating capability and better profitability outlook. Bloomberg reported that CATL is working with Tesla on a fast-charging battery in the US, which would present new progress in CATL’s tie-ups with North American local OEMs. Also, Xiaomi’s SU7 Pro launched in March 2024 adopted CATL's 101kWh Qilin battery pack. SU7’s successful launch showcased CATL as an efficient enabler of EV startups and a definer of battery pack systems.21

Preview

We remain positive on the long-term growth potential for the EV and battery value chain, along with the upward global EV penetration trajectory. Domestic old car replacement demand and export sales should support China’s resilient auto momentum and benefit leading domestic brands. We expect the China auto market to stay competitive in 2024 with a strong new product line-up from EV brands and new entrants such as Xiaomi. Though intensifying competition among EV brands remains the key concern with major EV brands announcing fierce price cuts in the past 2 months, we are seeing a rapid consumer interest rebound for key EV models22 after price cut announcements, which should be a leading indicator for sales and further drive up EV penetration. In addition, recent signs of the battery inventory cycle bottoming out after destocking last year imply a normalized industry landscape that could lead to a better margin profile for battery industry leaders.

China Clean Energy

Industry Update

- Solar – Polysilicon and supply chain prices further stabilized: Solar polysilicon prices were RMB 68/kg by the end of March, staying flat compared to one month ago23. Increasing polysilicon supply and inventory pressure from wafers could weigh on polysilicon prices going forward. Module prices remain the same as last month. Solar cell and module export volume was up 49% YoY in Feb, which could further accelerate in 2Q with the destocking in EU nearing completion in 1Q.24 Solar glass prices were flat MoM and Inventory levels decreased to 21.59 days from 28.56 days in the previous month, implying demand recovery. Inverter exports value was US$ 0.45bn in February, down 48% YoY. Inverter demand could recover in 2Q24 with the ongoing destocking process25.

- Grid and power installation – Strong wind and solar installations; grid Capex delivered mild growth: China’s Jan-Feb 2024 wind installations reached 9.9GW, +69% YoY. Jan-Feb 2024 solar installations were 36.7GW, +80% YoY. In Jan-Feb 2024, the electricity grid spending in China reached RMB 32.7bn. +2.3% YoY.26 The National Development and Reform Commission and National Energy Administration jointly issued on 1 March the Guidance on high-quality development for the power grid distribution network. It sets multiple medium-term (by 2025) and long-term (by 2030) targets for improving the smartness and stability of the distribution power grid.

Stock Comments

- Sungrow (300274 CH): Sungrow’s share price grew by +18% in March, a positive contribution to the index. Sungrow displayed more resilient profitability compared to other peers in Solar industries, thanks to the more benign market conditions and less intense competition of solar inverter space compared to the main solar supply chain. Sungrow is poised to benefit from the global solar demand growth and further expand its market share for inverters globally.27 Its Energy Storage System shipments will continue to grow by 50% YoY in 2024 with a stable margin, driven by global ESS demand growth under lower lithium costs.28

Preview

We are optimistic about the structural growth profile in renewable development, with China taking the leading position globally, particularly in the solar supply chain. However, it is worth noting that the solar supply chain entered a consolidation phase starting in 2023, as it has taken time for the industry to digest excess capacity in the past few years. We believe the profitability for the value chain will stay constrained, and players who can keep a good balance sheet and maintain technology leadership will be the long-term winners. We are bullish on the electrical equipment players who benefit from increased grid and system investment in China and globally. They enjoyed a higher selling price and volume growth amid global equipment tightness.

China Consumer Brand

Industry Update

- Some of the economists on the street including Goldman Sachs and Morgan Stanley raised China’s 2024 real GDP forecast on stronger than expected exports and manufacturing capex. March PMI beat the street expectation ring 1.7pt to 50.8 thanks to policy support for infrastructure capex and manufacturing upgrades. Service PMI also edged up 1.4pt with stronger production-related services, but consumption-related service PMI slipped. Overall domestic demand remains weak and deflationary pressures remain. Meanwhile, the market now expects less chance for additional easing from the end-April Politburo meeting as real GDP growth is tracking at 5%yoy in 1Q24.29

- While consumer sentiment remains weak, the Qingming festival (4-6 April) came in as a positive surprise. The number of domestic trips came in 11.5% above the 2019 level and spending per trip also has improved to above 2019 levels for the first time since the pandemic. According to China Tourism Group Duty-Free, they are seeing improving international shopper conversion rates and average per shopper spending. We are carefully watching out whether these are early signs of some recovery in household consumption trends.

Stock Comments

- Techtronic Industries (+26.19%) was the major contributor in March thanks to strong 2H23 earnings results. Revenue grew +10%yoy which beat earlier guidance of +5% on stronger than expected Milwaukee Pro segment. Management continues to keep 2024 guidance for mid to high single-digit growth along with Gross Profit Margin expansion by 40-60bps. The market is positive on the company’s next phase of growth, led by heavy-duty and intelligent product innovation which helps its flagship Milwaukee brand to drive double-digit revenue growth over the coming five years.30

- Li Auto (-33.50%) was the major detractor in March as the company announced to revise down its 1Q24 delivery guidance to 76K-78K units from 100K-103K units previously, due to lower than expected order intake. This implies 25K-27K unit volume sales in March, much weaker than the previous guidance of 50K units primarily on Mega’s demand was below expectation and customers adopted wait-and-see mode towards new L7/L8/L9. Meanwhile, the company also lowered its full-year guidance to 564K-639K units (+50-70% YoY) from previously 650K-800K(+70-115% YoY). The expectation has now reset and the next catalyst to watch out for would be its L6 launch around Beijing Auto Show in April 2024.

Preview

China’s economy has had a strong start to the year thanks to robust exports and manufacturing capex. Yet, this means there may be less chance for fiscal easing beyond the equipment capex upgrading incentives. While we have seen some indications of household consumption trends during the festival period, overall consumer confidence remains weak. Property market recovery may support consumption recovery but this also remains subdued at this moment.

China Cloud Computing

Industry Update

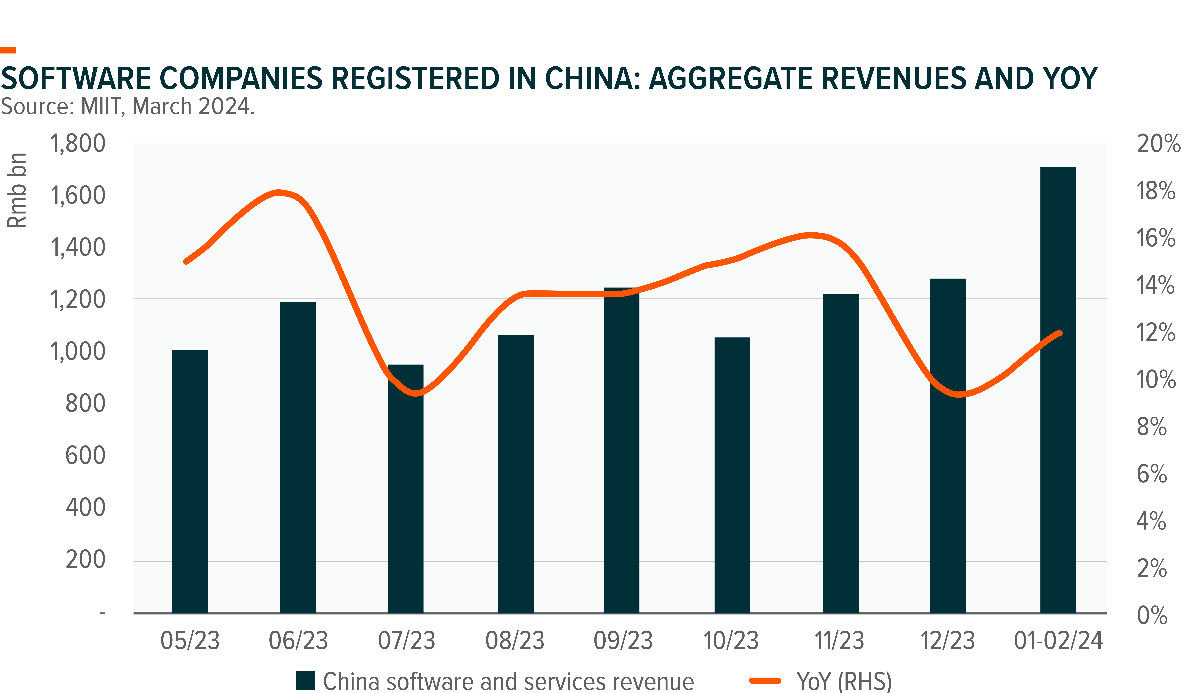

- China Software industry Jan and Feb 2024 revenues were +8.4% YoY, similar to the growth rate of December 2023. Revenue from software products +8.4% YoY to RMB 394.4bn during this period, while revenue from industrial software products +8.2% YoY to Rmb40.6bn. Cloud computing and big data services revenue +13.8% YoY, and e-commerce platform technical services revenue +3.8% YoY.31

Stock Comments

Key Contributors:

- Tencent (+10.47%): Tencent concluded 4Q23 with largely in-line 4Q revenue and a net profit beat (+44% YoY), alongside improving shareholder returns with upsized regular dividends and buyback. Mobile DnF is expected to be released in 2Q24, driving domestic mobile game revenue growth.32

- Beijing Kingsoft Office (+10.35%): KSO held the WPS AI Enterprise launch event on April 9th. During the event, the management introduced (1) a major upgrade of WPS Office, (2) new functionalities of WPS AI Enterprise, and (3) AI features of WPS collaboration. WPS AI Enterprise focuses on digital asset management (e.g., documents and chat history) and operating efficiency enhancement by replacing repetitive and routine work with AI. Grey testing of WPS AI for to-C started in late March 2024, with newly introduced WPS AI membership and WPS VIP, both of which support AI functions. The standard price for WPS AI member / WPS VIP is set at RMB 248 / RMB 348 per year (excluding discount), compared to RMB 148 / RMB 248 for WPS SVIP (basic) / WPS SVIP (pro).33

Key Detractors:

- Shanghai Baosight (-17.80%): The share price of Baosight was weak while CSI 300 was up 3% as 4Q23 revenue declined 25% YoY, missing market expectations, likely driven by software project delay with its parent and IDC weakness. 2023 connected transactions were down 2% YoY, much lower than the guidance.34

Preview

China software companies have concluded earnings reporting for 4Q23. 4Q23 industry revenue growth deteriorated from a low base. The forward-looking information is mixed with muted 2024 guidance and order book. IT spending of SOEs remains relatively more resilient than that of SMEs amid macroeconomic headwinds. On the other hand,

generative AI deployment has progressed faster than expected in various sectors, driving accelerated enterprise digitalization. We expect AI adoption to help increase productivity and optimize operational efficiency in the future, which means that there are potentially new growth drivers and improving margin for major software companies.

1Nvidia, March 2024

2Samsung Electronics, March 2024

3Naura, March 2024

4Mirae Asset, March 2024

5Mirae Asset, March 2024

6China Machinery Industry Federation, March 2024

7China Customs, March 2024

8Zhejiang Dingli Machinery, March 2024

9Wall Street Journal, March 2024

10CPCA, April 2024

11Goldman Sachs, April 2024

12UBS, March 2024

13UBS, March 2024

14UBS, March 2024

15Goldman Sachs, April 2024

16Company data, April 2024

17Morgan Stanley, April 2024

18Company data, March 2024

19UBS, March 2024

20UBS, March 2024

21Morgan Stanley, April 2024

22UBS, March 2024

23UBS, March 2024

24UBS, March 2024

25UBS, March 2024

26National Energy Administration, March 2024

27UBS, March 2024

28UBS, March 2024

29Mirae Asset, March 2024

30Techtronic Industries, March 2024

31MIIT, March 2024

32Tencent, March 2024

33Beijing Kingsoft Office, March 2024

34Shanghai Baosight, March 2024

Disclaimer & Information for Investors

No distribution, solicitation or advice: This document is provided for information and illustrative purposes and is intended for your use only. It is not a solicitation, offer or recommendation to buy or sell any security or other financial instrument. The information contained in this document has been provided as a general market commentary only and does not constitute any form of regulated financial advice, legal, tax or other regulated service.

The views and information discussed or referred in this document are as of the date of publication. Certain of the statements contained in this document are statements of future expectations and other forward-looking statements. Views, opinions and estimates may change without notice and are based on a number of assumptions which may or may not eventuate or prove to be accurate. Actual results, performance or events may differ materially from those in such statements. In addition, the opinions expressed may differ from those of other Mirae Asset Global Investments’ investment professionals.

Investment involves risk: Past performance is not indicative of future performance. It cannot be guaranteed that the performance of the Fund will generate a return and there may be circumstances where no return is generated or the amount invested is lost. It may not be suitable for persons unfamiliar with the underlying securities or who are unwilling or unable to bear the risk of loss and ownership of such investment. Before making any investment decision, investors should read the Prospectus for details and the risk factors. Investors should ensure they fully understand the risks associated with the Fund and should also consider their own investment objective and risk tolerance level. Investors are advised to seek independent professional advice before making any investment.

Sources: Information and opinions presented in this document have been obtained or derived from sources which in the opinion of Mirae Asset Global Investments (“MAGI”) are reliable, but we make no representation as to their accuracy or completeness. We accept no liability for a loss arising from the use of this document.

Products, services and information may not be available in your jurisdiction and may be offered by affiliates, subsidiaries and/or distributors of MAGI as stipulated by local laws and regulations. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Information for EU investors pursuant to Regulation (EU) 2019/1156: This document is a marketing communication and is intended for Professional Investors only. A Prospectus is available for the Mirae Asset Global Discovery Fund (the “Company”) a société d'investissement à capital variable (SICAV) domiciled in Luxembourg structured as an umbrella with a number of sub-funds. Key Investor Information Documents (“KI(I)Ds”) are available for each share class of each of the sub-funds of the Company.

The Company’s Prospectus and the KI(I)Ds can be obtained from www.am.miraeasset.eu/fund-literature . The Prospectus is available in English, French, German, and Danish, while the KI(I)Ds are available in one of the official languages of each of the EU Member States into which each sub-fund has been notified for marketing under the Directive 2009/65/EC (the “UCITS Directive”). Please refer to the Prospectus and the KI(I)D before making any final investment decisions.

A summary of investor rights is available in English from www.am.miraeasset.eu/investor-rights-summary/.

The sub-funds of the Company are currently notified for marketing into a number of EU Member States under the UCITS Directive. FundRock Management Company can terminate such notifications for any share class and/or sub-fund of the Company at any time using the process contained in Article 93a of the UCITS Directive.

Hong Kong: It is intended is for Hong Kong investors. Before making any investment decision to invest in the Fund, Investors should read the Fund’s Prospectus and the information for Hong Kong investors (of applicable) of the Fund for details and the risk factors. The individual and Mirae Asset Global Investments (Hong Kong) Limited may hold the individual securities mentioned. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Securities and Futures Commission.

Singapore: It is not intended for general public distribution. The investment is designed for Institutional investors and/or Accredited Investors as defined under the Securities and Futures Act of Singapore. This document is issued by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Monetary Authority of Singapore. Please consult with your professional adviser for further information on the availability of products and services within your jurisdiction.

Australia: The information contained in this document is provided by Mirae Asset Global Investments (HK) Limited (“MAGIHK”), which is exempted from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) (Corporations Act) pursuant to ASIC Class Order 03/1103 (Class Order) in respect of the financial services it provides to wholesale clients (as defined in the Corporations Act) in Australia. MAGIHK is regulated by the Securities and Futures Commission of Hong Kong under Hong Kong laws, which differ from Australian laws. Pursuant to the Class Order, this document and any information regarding MAGIHK and its products is strictly provided to and intended for Australian wholesale clients only. The contents of this document is prepared by Mirae Asset Global Investments (HK) Limited and has not been reviewed by the Australian Investments & Securities Commission.

Swiss investors: This document is intended for Professional Investors only. This is an advertising document. The Swiss Representative is 1741 Fund Solutions AG, Burggraben 16, CH-9000 St. Gallen. The Swiss Paying Agent is Tellco AG, Bahnhofstrasse 4, CH-6431 Schwyz. The Prospectus and the Supplements of the Funds, the KI(I)Ds, the Memorandum and Articles of Association as well as the annual and interim reports of the Company are available free of charge from the Swiss Representative.

UK investors: This document is intended for Professional Investors only. The Company is a Luxembourg registered UCITS, recognised in the UK under section 264 of the Financial Services and Markets Act 2000. Compensation from the UK Financial Services Compensation Scheme will not be available in respect of the Fund. The taxation position affecting UK investors is outlined in the Prospectus. This document has been approved for issue in the United Kingdom by Mirae Asset Global Investments (UK) Ltd, a company incorporated in England & Wales with registered number 06044802, and having its registered office at 4th Floor, 4-6 Royal Exchange Buildings, London EC3V 3NL, United Kingdom. Mirae Asset Global Investments (UK) Ltd. is authorised and regulated by the Financial Conduct Authority with firm reference number 467535.

Copyright 2025. All rights reserved. No part of this document may be reproduced in any form, or referred to in any other publication, without express written permission of Mirae Asset Global Investments (Hong Kong) Limited.